Why Your Mortgage Pre-Approval Shrank: DTI Math You Can Run with AI

Your pre-approval was fine three months ago and now the number dropped. The usual suspects: a rate that crept from 6.4% to 6.49%, a new car payment, and the 28/36 DTI rule doing exactly what it was built to do. Here is the math lenders run, plus a copy-paste AI prompt that runs it for you in five minutes.

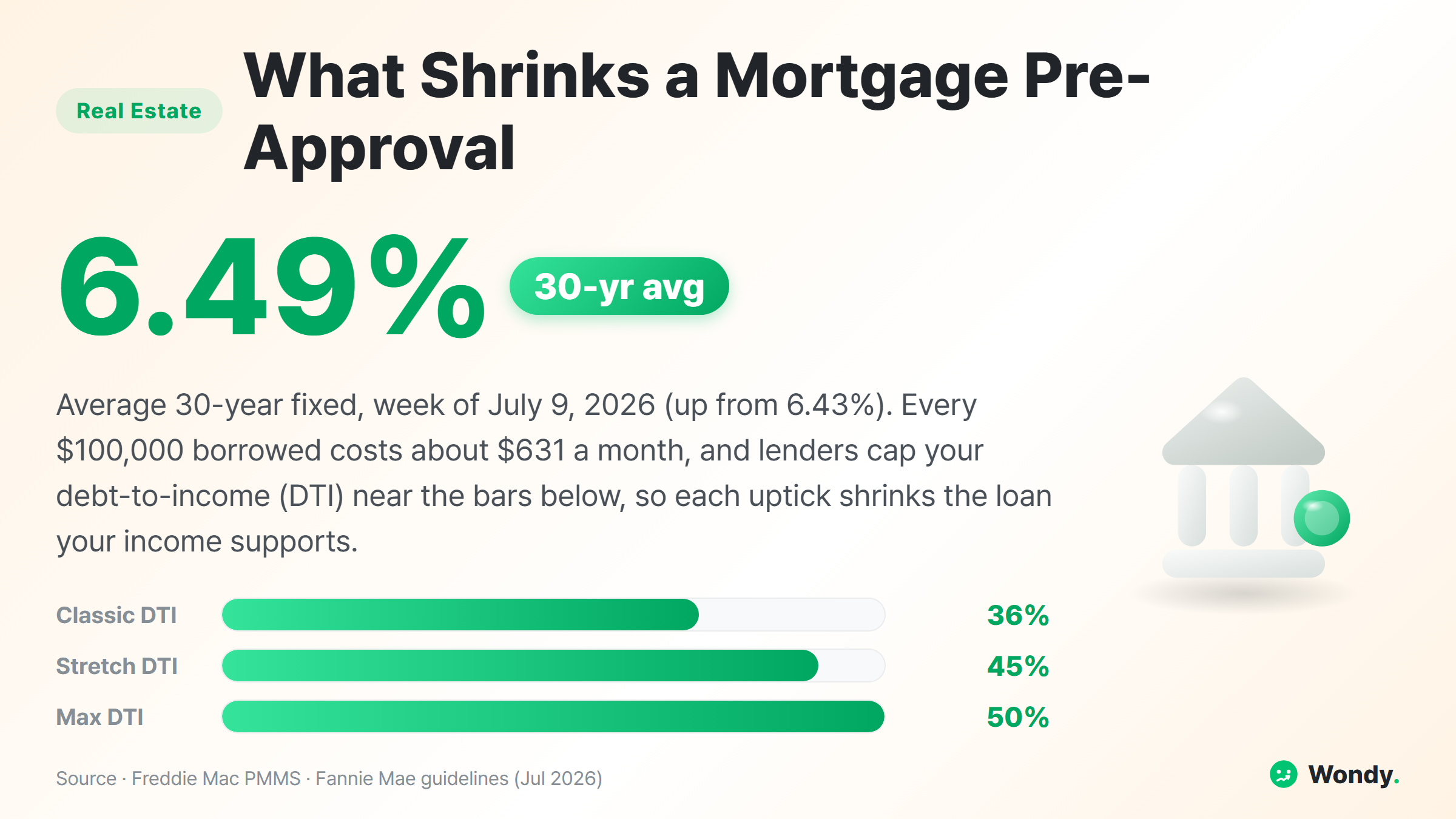

On July 9, Freddie Mac's weekly survey put the average 30-year fixed at 6.49%, up from 6.43% the week before. Six hundredths of a point sounds like rounding error, until it lands on a pre-approval letter. If you got pre-approved in spring and came back to lock this month, there is a decent chance the lender quoted you a smaller number, and nothing about your life changed.

It feels like a bait and switch. It almost never is. A pre-approval is a snapshot, not a promise, and three inputs behind it move constantly. Once you know the formula, you can recheck your own number any week you want, with AI doing the arithmetic.

Suspect 1: the rate moved, even a little

Freddie Mac's weekly survey put the average 30-year fixed at 6.49% for the week of July 9, 2026, up from 6.43% the week before. A year ago it was 6.72%. These look like tiny wiggles, but pre-approvals are leveraged to them.

Here is the plain-English version. At 6.49%, every 631 a month in principal and interest over 30 years. When the rate ticks up, that per-$100k cost rises, and since your monthly budget is fixed by your income, the loan size that fits inside it shrinks. Rate up, borrowing power down, automatically. Your lender did not change their mind. The market changed the input.

Suspect 2: DTI, the ratio that runs the show

DTI, debt-to-income ratio, is the percentage of your gross monthly income that goes to debt payments. Lenders read it two ways. Front-end: your housing payment alone, ideally under 28% of income. Back-end: housing plus every other debt (car, student loans, credit card minimums), ideally under 36%. That pair is the classic 28/36 rule.

Real-world ceilings are looser than the classic rule. Conventional loans routinely go to 45% back-end, and automated underwriting can approve up to 50% with strong credit and reserves. FHA runs about 31/43 standard with similar stretch room. But every point above 36% costs you options and pricing, so the 36% line is still the number to plan around.

This is where "nothing changed" usually turns out false. Financed a car in May? That 631 per 450 payment is roughly $71,000 of home-buying power. One car, gone from the house.

- $7,900/mo gross income

- 36% DTI budget: $2,850

- All of it available for housing

- Same $2,850 DTI budget

- Housing budget drops to $2,400

- Roughly $71k less loan at 6.49%

Suspect 3: your pre-approval simply expired

Pre-approval letters typically last 60 to 90 days. After that, the lender re-pulls credit, re-verifies income, and re-runs the math at current rates. If rates rose or debts appeared during your house hunt, the refreshed letter prints smaller. Nothing personal, just a new snapshot with new inputs.

I ran this myself: the AI affordability check

The formula is: gross monthly income × 0.36, minus existing debt payments, equals your PITI budget (principal, interest, taxes, insurance). Then divide what is left after taxes and insurance by the per-$100k payment. Doable by hand, faster by chatbot. Paste this into ChatGPT or Claude and swap the brackets:

You are a mortgage affordability calculator. Estimate my pre-approval range.

- Gross annual income: [$95,000]

- Monthly debt payments (car, student loans, cards): [$750]

- Current 30-year fixed rate: [6.49%]

- Down payment saved: [$30,000]

- Estimated monthly property tax + insurance for my target area: [$550]

Show your work step by step:

1. Monthly gross income, and my 36% back-end DTI budget

2. Subtract my debts: what is left for PITI

3. Subtract tax + insurance: what is left for principal & interest

4. At 6.49% over 30 years, the loan size that P&I supports

5. Loan + down payment = rough max purchase price

6. Repeat at 45% DTI so I can see the aggressive-lender version

End with one line on why an actual lender's number will differ

(credit score, rate lock date, lender overlays).

With my example inputs, here is what came back.

1. Income & budget: 7,917/mo gross. 36% DTI budget = $2,850.

2. Minus debts: 750 = $2,100 for PITI.

3. Minus tax + insurance: 550 = $1,550 for principal & interest.

4. Loan size: at 6.49%/30yr, P&I is ~100k → 245,000 loan**.

5. Max price: 30,000 down ≈ $275,000 purchase price.

6. At 45% DTI: budget 358,000 loan / $388,000 price**, if a lender approves the stretch.

Note: your actual pre-approval depends on credit score, the rate on your lock date, and lender-specific rules, so treat this as a planning range.

Two things worth noticing in that answer, using my example numbers. First, the spread between the 36% and 45% versions is over 100k payment figure. That is the one number I always verify by hand against any online mortgage calculator before trusting the rest.

Where the AI sketch ends and the lender begins

The chatbot cannot see your credit score, and pricing changes meaningfully across score bands. It does not know your lender's overlays, the extra rules banks stack on top of Fannie Mae and FHA minimums. And it is only as current as the rate you type in, so grab the fresh weekly average from Freddie Mac's survey before each run. Use the AI to know which lever is squeezing you, rates, debts, or the DTI cap, then bring that literacy to a loan officer for the real number.

FAQ

Why did my mortgage pre-approval amount go down?

Three things move it: rates, debts, and re-verification. A higher rate raises the cost per dollar borrowed, so the same income supports a smaller loan. Any new debt payment eats your DTI budget directly. And pre-approvals expire in 60 to 90 days, so lenders re-run everything with current inputs.

What DTI do I need for a mortgage in 2026?

The classic guide is the 28/36 rule: housing under 28% of gross monthly income, total debts under 36%. Conventional loans can stretch to 45% and up to 50% back-end with strong credit and automated underwriting; FHA runs about 31/43 standard with stretch room. Lower is safer and prices better.

How much house can I afford on my salary?

Work backward from DTI: gross monthly income × 0.36, minus debt payments, is your rough PITI budget. At July 2026's average 6.49% rate, every 631 a month in principal and interest, so divide your P&I budget by 631 and multiply by 100,000 for the loan size.

Can AI calculate my mortgage pre-approval amount?

It approximates well if you feed it income, debts, the current rate, and down payment. It shows the full calculation, which is the real value: you learn which input is the bottleneck. Actual pre-approvals depend on credit, documentation, and lender overlays, so confirm with a loan officer.

Disclaimer

This article explains how lenders calculate affordability so you can sanity-check your own numbers. It is not financial advice and does not guarantee any loan amount or rate. Figures are as of July 13, 2026 and will change; verify current rates and program rules with a licensed lender before making decisions.

Sources

- Freddie Mac, Primary Mortgage Market Survey (30-yr avg 6.49%, week of July 9, 2026): https://www.freddiemac.com/pmms

- FRED, 30-Year Fixed Rate Mortgage Average in the United States: https://fred.stlouisfed.org/series/MORTGAGE30US

- Bankrate, "What Is a Debt-to-Income Ratio for a Mortgage?" (28/36 rule): https://www.bankrate.com/mortgages/why-debt-to-income-matters-in-mortgages/

- Fannie Mae Selling Guide, Debt-to-Income Ratios (B3-6-02): https://selling-guide.fanniemae.com/

- Consumer Financial Protection Bureau, "What is a debt-to-income ratio?": https://www.consumerfinance.gov/ask-cfpb/what-is-a-debt-to-income-ratio-en-1791/